Morgan Stanley (NYSE:)’s latest analysis paints a nuanced picture of the Indian consumer industry, leading to a revision of their view from ‘attractive’ to ‘in-line’. Despite a favorable outlook for GDP growth driven by cyclical businesses, the defensive consumer sector is expected to lag due to increased competition and changing consumer behavior.

The report highlights several key factors contributing to this shift. Increased competition in the home and personal care (HPC) segment, driven by pricing, product and distribution strategies, is expected to continue. This, combined with lower growth expectations and rich valuations, will likely lead to a downgrade in the consumer sector.

Offer: Unlock the true value of stocks with InvestingPro by click here – your ultimate stock analysis tool! Say goodbye to inaccurate valuations and make informed investment decisions with accurate intrinsic value calculations. Buy it now at a limited time discount of 69%, only INR 216/month!

Ridham Desai, Morgan Stanley’s Indian stock market strategist, highlights the continued recovery of the Indian economy. However, this upward cycle poses challenges for basic stocks, with cyclical consumption outperforming defensive stocks. Projections indicate GDP growth of 6.8% and 6.5% in FY25 and FY26 respectively, supported by a recovery in capital expenditure.

In the context of this cyclical upturn, the consumer staples sector is expected to underperform due to their defensive nature. Similar trends were observed in the 2003-2007 cycle, when basic inventories lagged significantly as the economy strengthened.

While consumption remains a pillar of India’s economic growth, the post-pandemic recovery has been uneven, especially in rural areas. Factors such as a shift towards services, a slower recovery in rural demand and continued adjustments in household budgets are contributing to this mixed growth outlook.

Remove ads

.

However, there is optimism about a gradual recovery in consumption growth, supported by factors such as inflation moderation, the resilience of the rural sector and improving labor market conditions. This is consistent with India’s long-term consumption story as outlined in Morgan Stanley’s BluePaper, which predicts continued consumption growth and a shift to discretionary spending as income levels rise.

While challenges in the consumer sector persist, India’s consumption story remains intact, poised for growth as the economy develops and consumer preferences change. Morgan Stanley’s analysis provides valuable insights for investors navigating the dynamic landscape of the Indian consumer industry.

Some consumer stocks that investors should remain cautious about due to their overvaluation are:

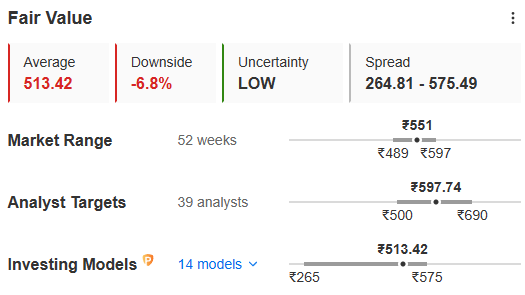

Image source: InvestingPro+

Dabur India (NS:) – The stock has returned a paltry 7.3% over the past year, despite appearing overvalued at 6.8%. Even 39 analysts tracking this counter are not too optimistic and give a slight edge up to INR 597.

Image source: InvestingPro+

Hindustan Unilever (LON:) (NS:) is again an underperformer with an annual return of -8.43%. ProTips raises a plethora of red flags on the valuation front and the fair value after analyzing the stock against 14 different financial models is INR 2,214, overvalued by 6.4%.

InvestingPro, the ultimate stock analysis tool, is now at your fingertips at a discount of up to 69%, offering unparalleled insights for just INR 216 per month, but hurry, this offer won’t last long! click here to grab your offer

Also read: Driving Growth: Understanding the Indian Car Dealership Landscape

Remove ads

.

X (formerly Twitter) – Ayush Khanna